Sector Spotlight: Specialist Healthcare

How has M&A fared in the Specialist Healthcare sector in recent months?

The specialist healthcare M&A sector in the UK has been buzzing with activity in recent months, presenting a blend of challenges and successes.

One of the foremost challenges can be navigating the complex regulatory environment. The UK Competition and Markets Authority (CMA) has been vigilant in recent years in scrutinizing deals to prevent monopolistic practices and ensure fair competition. This heightened scrutiny can delay approvals and create uncertainty for companies, as seen in the protracted review of the merger between Circle Health and BMI Healthcare in 2019 with investigations continuing well after the transaction had completed. The CMA’s intervention, aimed at preventing reduced patient choice, underscores the regulatory hurdles that can complicate M&A activities.

Financial constraints also pose a significant challenge. The economic impact of the COVID-19 pandemic continues to strain healthcare budgets, making it harder for smaller entities to sustain operations independently. These financial pressures are driving many healthcare providers to seek mergers as a survival strategy. For example, the 2021 acquisition of the UK-based care home operator HC-One by Safanad and Court Cavendish highlights how financial instability can spur consolidation. This deal aimed to stabilise HC-One’s operations and ensure continued care for its residents by leveraging the resources and expertise of its new owners.

Despite these challenges, the UK specialist healthcare sector has seen notable successes in the last decade. One such success is the acquisition of Care Fertility in 2022, one of the UK’s leading fertility treatment providers, by Nordic Capital, a private equity firm. This deal aimed to expand Care Fertility’s network of clinics and enhance their technological capabilities, improving patient outcomes in the fertility treatment sector.

Technological advancements are also fuelling successful M&A transactions. Companies that integrate innovative technologies into their healthcare services are particularly attractive to investors. For instance, the acquisition of Push Doctor by Square Health 2 years ago is a prime example of leveraging technology to enhance healthcare delivery. Push Doctor, known for its tele-health services, merged with Square Health to provide a more integrated digital health platform, aiming to offer patients a seamless blend of online consultations and traditional healthcare services.

In summary, while the specialist healthcare M&A sector in the UK faces challenges like regulatory scrutiny and financial pressures, it is also experiencing significant successes. Strategic mergers, technological integration, cross-border transactions, and a focus on specialised care are driving growth and innovation. These trends showcase the sector's resilience and its potential for continued transformation, promising a dynamic future for healthcare M&A in the UK.

The following graphics & excerpts are from the First Page Sage report detailing Healthcare EBITDA & Valuation Multiples for 2023/2024:

During the research period, our analysts made the following observations about the current healthcare M&A market:

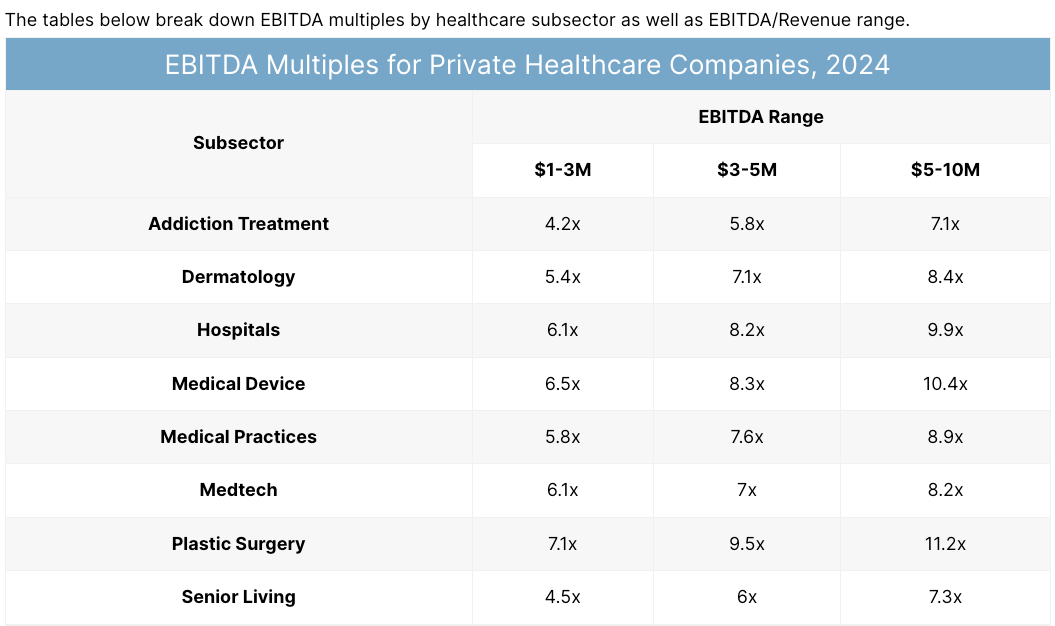

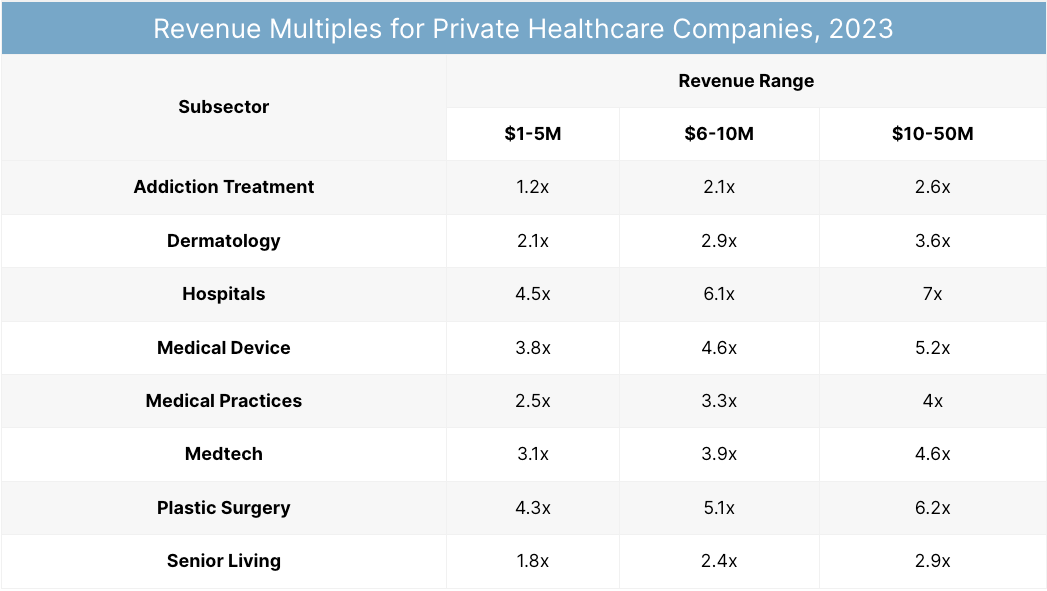

- The subsectors with the highest multiples were non-essential healthcare companies: plastic surgery and medical devices. However, those industries have seen more inconsistency in valuations over time, rising and falling with major economic indicators.

- The subsectors with the lowest multiples – but greater long-term stability in valuations – were addiction treatment and senior living, which tend to be viewed as slower growth businesses tied to physical real estate.

- On average, companies represented by M&A advisors or investment banks saw a 23% higher multiple from buyers.

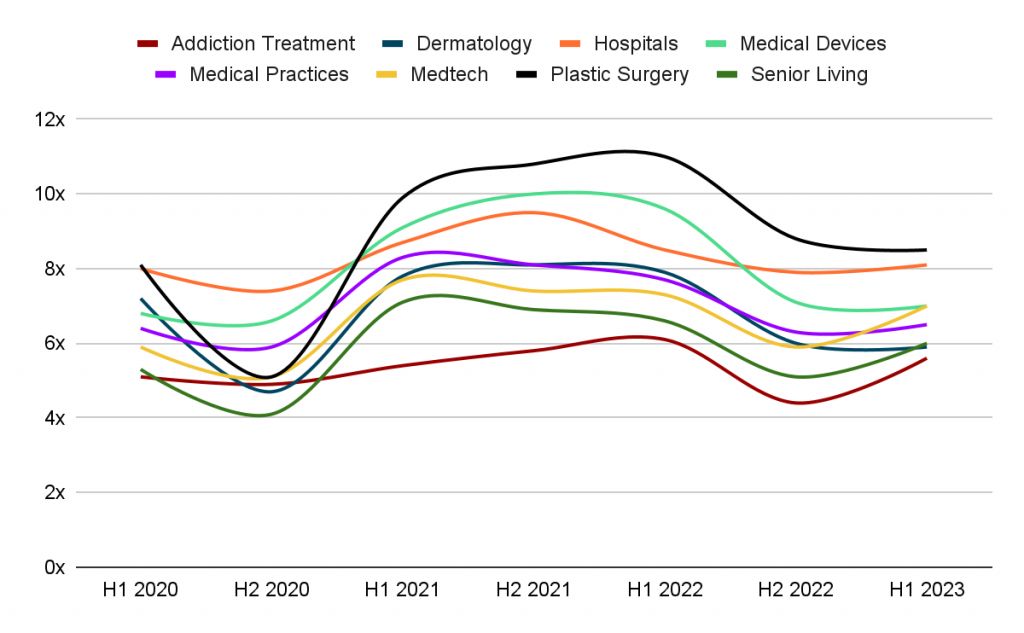

EBITDA Multiples for Private Healthcare Companies, 2020-2024:

With the industry’s excellent performance (compared to other industries) in the current economic down-cycle, and with more uncertainty ahead, we expect healthcare companies will continue to see high valuations and deal volume through the end of 2024.

The State of Healthcare M&A in 2024

Unlike other industries which saw declines from the macroeconomic turbulence of H2 2022, healthcare saw only minor losses—making it one of the highest performing sectors during the last year. There was a notable disparity in valuation between essential vs. non-essential healthcare companies. More stable subsectors like hospitals weathered the storm remarkably well, experiencing an ~7% reduction in EBITDA multiples, from 8.5x to 7.9x, while less essential healthcare specialties like plastic surgery experienced a more severe decline of ~20% in the same time span, from 11x to 8.8x.

While 2022 was a record year in healthcare M&A, deal volume slowed a bit in 2023, dropping 17% between Q3 2022 and Q3 2023. However, despite the decline in deal volume, multiples were climbing their way back up to 2021 levels, painting a picture of a 2024 M&A environment in which buyers are pickier about transactions, but willing to pay higher amounts.

Deal Volume Will Rise

Because of the economic downturn in H2 2022, many buyers chose to hold off on purchasing decisions until they were able to get a better sense of the macroeconomic outcome. As a result, there has been a great deal of dry powder in the hands of buyers which has not yet been deployed. As the economy improves, we expect this dry powder will be used quickly as buyers attempt to grow their businesses.

Private Equity Will Focus on Middle Market Companies

With the margins for error being as high as they are due to economic uncertainty, private equity companies are more likely to prioritize the purchase and sale of smaller portfolio companies due to the greater amount of profit which can be extracted from their eventual sale. Activity amongst these buyers saw a slight decline at the end of 2022, but came back in late 2023, indicating an intent to capitalize on the existing stability while it lasts.

More News & Deals...

Our 'Focus On' Resource Series...