UK M&A Market Activity H1-2023

The latest Experian Market IQ Report was published recently, detailing UK M&A activity for H1-2023.

At first glance, the reporting doesn't look too encouraging but the lack of 'mega deals' (worth £5bn+) is a huge contributing factor. Let's look at the numbers...

With inflation and rising interest rates hitting the headlines on a daily basis, it's no surprise the impact this would have on the UK M&A market as a whole. At the larger end of the market there have been significantly fewer transactions and lower deal values being achieved during H1.

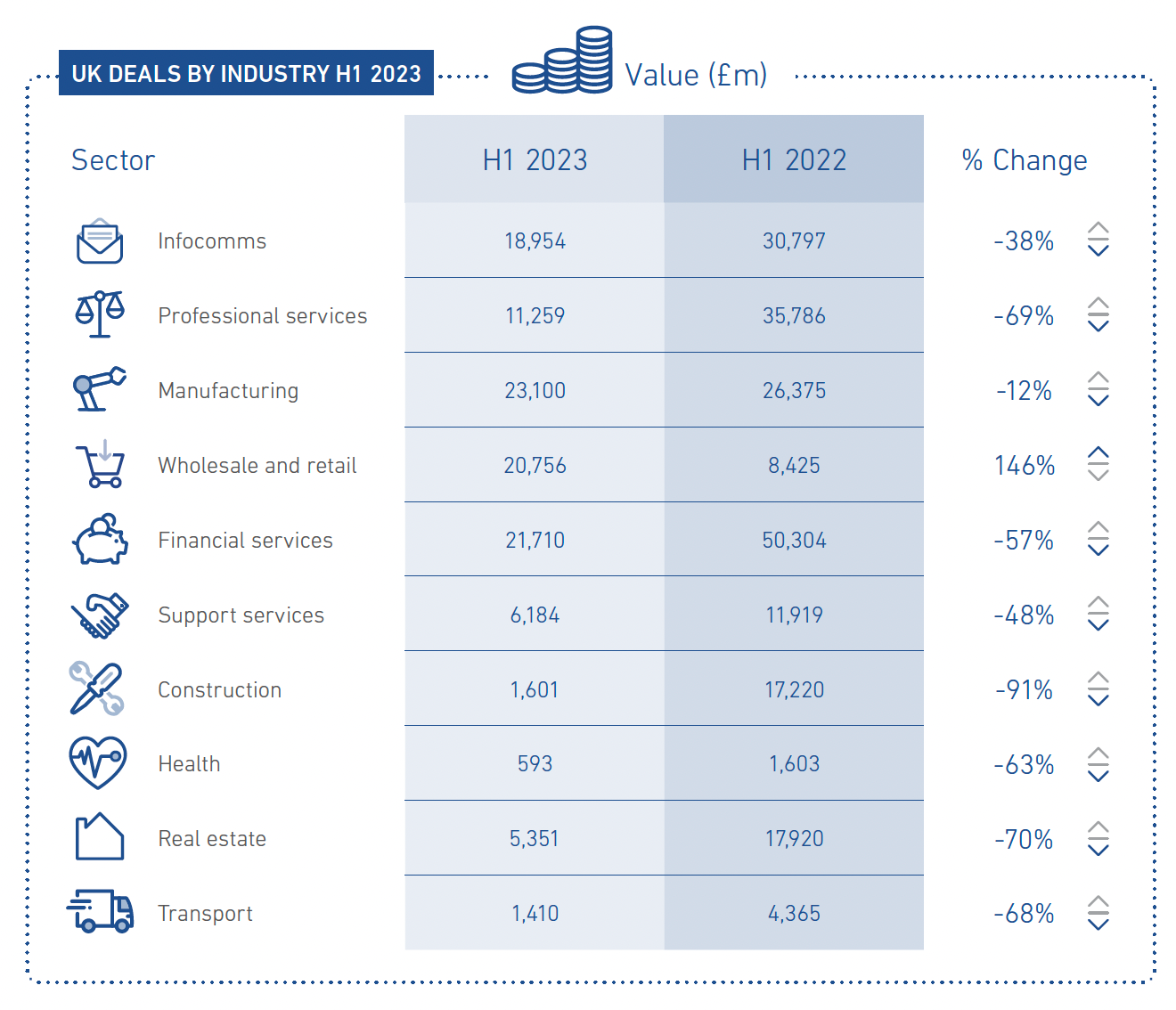

Let's look at Volume and Value by industry below:

Slightly skewing the figures is the one notable 'mega deal' which saw Dechra Pharmaceuticals Plc being acquired for £4.46bn - the largest deal so far this year.

LOWER & MID-MARKET

Does the lack of top-end deals reflect the whole market?

MarketIQ added the following comment in their report:

"An uncertain outlook meant that many UK companies looked to have put their M&A plans on hold in the near term and, following a prolonged period in which both cross-border corporate deal making and private equity investment in the UK boomed, both sources of activity declined in H1.

Increased interest rates have pushed up the cost of financing higher value transactions and, with potential acquirors also weighing up their ability to push through big ticket acquisitions in a more stringent regulatory environment, a shift towards smaller and mid-market M&A was apparent."

So, not all doom and gloom, especially for the lower mid-market in which we operate. 'Every cloud' etc.

An article in the Financial Times also backed up the numbers:

"Dealmakers are focusing their takeover efforts on the UK’s middle-market companies this year, attracted by lower prices that can make those transactions easier to stomach in a bumpy and unstable market.

At the same time, massive transactions have fallen domestically to a near halt, as persistent domestic inflation and rising interest rates make such deals more costly to finance. Antitrust regulators are also more aggressively challenging big acquisitions."

The same article also went on to state:

“Where we are off is those elephant-type deals,” said one senior UK banker. “It’s not like we’ve gone out to target smaller deals but that’s where the opportunities are.”

Companies and private equity groups are now focused on more manageable transactions.

“People are more focused on strategic low-risk, more bolt-on, ‘right down the middle of the fairway’ type deals,” added one UK M&A banker.

So far this year, 85 per cent of firm takeover offers for UK listed companies, or 23 deals in total, have been worth less than £500mn in equity value, according to data compiled by the investment bank Peel Hunt.

That is the highest ratio since the start of 2020 and a significant increase from last year, when about 55 per cent of takeovers were in that lower range.

Advisers are optimistic that next year could see a return to larger deals when there may be more stability in markets and the macroeconomic outlook settles.

“Into ‘24 we should see larger deals start to re-emerge,” added another top UK banker. “When it comes back, it’s going to come back with velocity.”

Sources FT.com and Experian MarketIQ

For the market La Salle operate in, this shift to mid-market deals presents more opportunities for our clients.

We have not witnessed a slow-down in the appetite of clients seeking a sale or exit in the current climate. What we have seen is a larger number of investors and trade buyers from the top end of the market looking at companies they may have previously deemed 'too small' for a strategic acquisition.

As always, should you be considering an exit or looking to sell your company, it's best to explore all the options available to you.

Here at La Salle, because we specialise in sell-side, we work closely with shareholders and company owners to evaluate the best options for you, the individual, to get the maximum return on your years of hard work.

Reach out today for an initial, informal chat to see how we can assist you.

All conversations are in complete confidence.

More News & Deals...

Our 'Focus On' Resource Series...